Back to blog

#35 - Strait of Hormuz paralyzed, India signs another deal and Stellantis under investigation

Edoardo Arbizzi

🌎 Global View

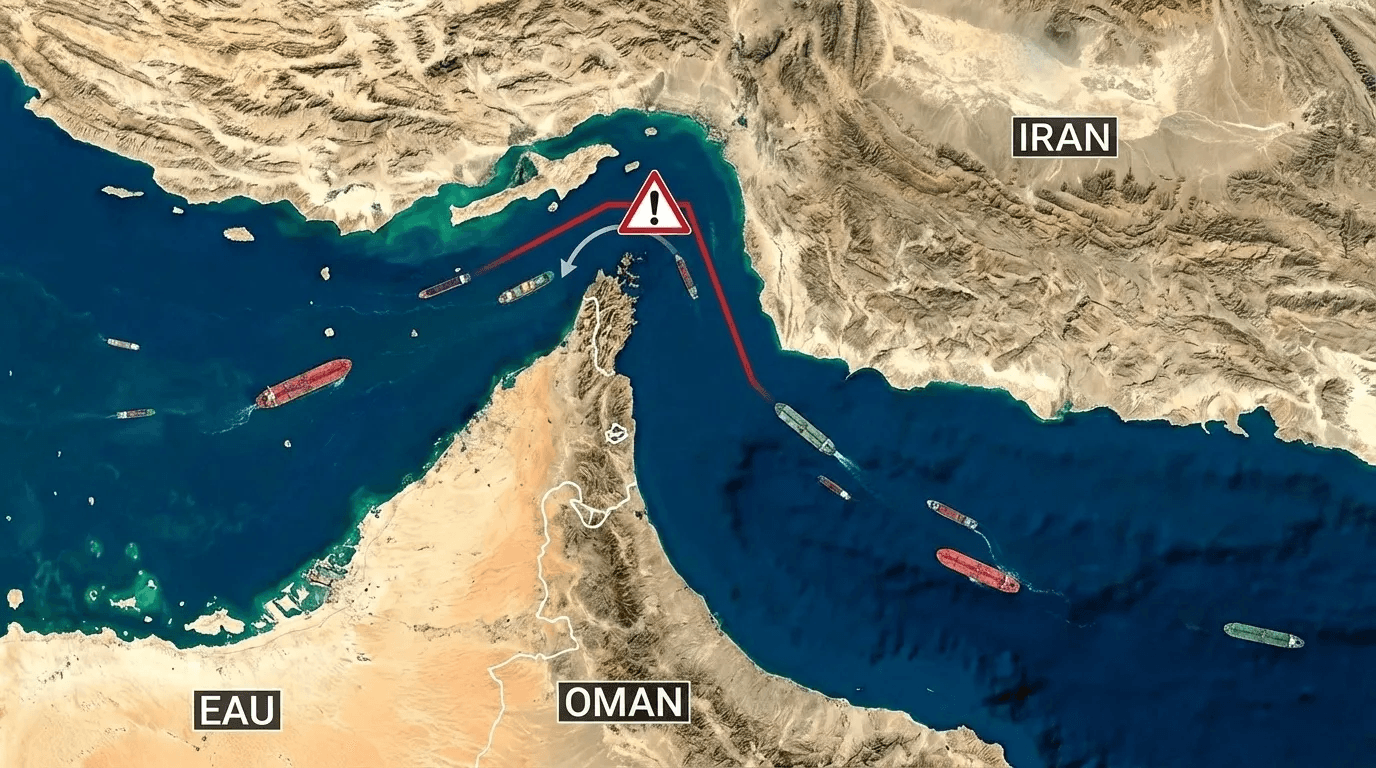

🚧🚢 The Strait of Hormuz is closed. The world pays.

On February 28, the US and Israel launched Operation Epic Fury against Iran. Within hours, the Revolutionary Guard blocked the strait: five tankers were hit, 150 vessels were stranded, and Maersk, MSC and COSCO suspended operations. The corridor was effectively sealed.

Why it is so alarming. Through that 20 mile stretch passed 31 percent of seaborne crude, 30 percent of European jet fuel, and one fifth of global LNG. Not only oil: aluminum, fertilizers, sugar. Each day of disruption meant 13 million barrels not reaching destination. A route of systemic importance.

Markets reacted immediately. Brent rose 13 percent in 48 hours, European TTF gas jumped 76 percent in a week, and rates for large crude carriers hit a historical record of $423,736 per day, up 94 percent over a single weekend. Goldman Sachs and Barclays warned that if the disruption had lasted more than two weeks, prices could have reached $100 per barrel. Some spoke of $120. For comparison, during the 2022 energy crisis TTF peaked at €340 per MWh. Today the system started from a more fragile position, with EU storage at 30 percent.

The risk was not evenly distributed. Saudi Arabia and the UAE had alternative pipelines, but with insufficient capacity to offset a total shutdown. Kuwait, Qatar and Bahrain had no viable alternatives. Japan and South Korea imported 75 percent and 70 percent of their oil from the Middle East, with LNG reserves covering only two to four weeks. China had strategic reserves estimated at 900 million barrels, almost three months of coverage, but a prolonged crisis would have forced it to compete on Atlantic markets. The unexpected winner? Russia, as India and China increased reliance on its crude.

The strait is technically open, but like an airport with all flights canceled. Major maritime insurers such as Gard, Skuld and the London P&I Club removed war risk coverage for the Persian Gulf. For a large tanker, a single percentage point increase in insurance equaled $2.74 million per voyage. Shipowners stayed put. The outcome was identical to a full physical blockade.

For Procurement the damage is already tangible. Rerouting via the Cape of Good Hope added 10 to 14 days to transit times and up to 30 percent to logistics costs. Automotive, pharmaceuticals, electronics: all sectors faced slowdowns or production stops. European gas intensive industries such as chemicals, fertilizers, steel and glass are already evaluating output cuts. If Hormuz and Suez were disrupted simultaneously, we would face a Covid level shock, or worse.

The Strait of Hormuz has been in risk registers for decades. Yet when it happened, most supply chains had no real plan B.

The question for Procurement Managers: do you have a real map of your single points of failure, or are you drawing it now under pressure?

🔗 Sources: Kpler, CNBC, Procurement Magazine

🇮🇳🇨🇦 India Canada uranium agreement

First the EU. Now Canada. India is building the energy supply chain of the future one contract at a time. On March 2, 2026, during the first bilateral visit of a Canadian Prime Minister to India since 2018, Mark Carney and Narendra Modi signed a Strategic Energy Partnership covering LNG, LPG, uranium, solar and hydrogen. At the center: Cameco, the world’s largest uranium company, will supply 22 million pounds of nuclear fuel to India from 2027 to 2035. Contract value: 2.6 billion Canadian dollars.

Why now. India’s declared objective is to reach 100 GW of nuclear capacity by 2047, twelve times current levels. The structural issue is clear: it currently produces around 600 tons of uranium per year, while projected demand exceeds 1,800 tons, a threefold gap. Domestic reserves are limited and low grade. With 1.4 billion people and industrialization accelerating faster than any other major economy, India cannot afford to depend on the spot market for reactor fuel. Without long term secured contracts, its nuclear ambition remains theoretical.

This is not just about uranium. The two countries signed six additional MoUs, aiming to increase bilateral trade from $13 billion to $50 billion by 2030, nearly four times current volumes. Cooperation on small modular reactors, next generation reactors, AI and semiconductors is also on the table. A separate MoU between India’s Ministry of Mines and Canada’s Department of Natural Resources covers the entire critical minerals value chain: exploration, extraction, processing and investment promotion. The uranium deal is the anchor. The rest is the network.

The bigger picture. This agreement is not isolated. It is part of a deliberate Indian strategy to diversify supply globally, built deal by deal, partner by partner. New Delhi understands that the next decade’s energy security is decided today in multi year contracts signed now. Cameco CEO Tim Gitzel confirmed the structural shift: sovereign buyers are locking in large volumes from multiple suppliers simultaneously, in a window where demand is rising and available supply is increasingly uncertain. Those who delay will find the market already allocated.

♻️ Sustainability Focus

🚗🔋 Stellantis lost $26 billion on EVs. Now suppliers pay the bill.

On February 6, 2026, Stellantis announced a $26.5 billion impairment linked to its EV strategy. The stock fell 28 percent in a single session, the worst day in its history. Management admitted EV adoption forecasts had been excessively optimistic. Three weeks later came the investigation: the law firm Levi & Korsinsky is examining whether public communications between Q3 2025 and February 6 accurately reflected the company’s internal understanding of the true state of its EV assets.

The supply chain bears the heaviest burden. Nearly $8 billion of the writedowns are cash payments to suppliers to compensate for canceled orders, spread over four years starting in 2026. These are not abstract figures: they represent terminated contracts, production capacity built on flawed forecasts, and specialized suppliers that invested in EV components now rendered redundant. The charges also include resizing the entire EV supply chain, revisions to contractual guarantees, and a net loss of $26.3 billion for 2025 compared to a $6.5 billion profit in 2024. One year. A $32 billion reversal.

This is not only about Stellantis. Ford announced $19.5 billion in EV writedowns, GM $7.6 billion, Volkswagen $6 billion. John Murphy of Haig Partners called it the single largest capital allocation mistake in automotive history, forecasting at least $100 billion in total sector writedowns. This is not an isolated corporate issue. It is a systemic demand forecasting failure built on assumptions the market never validated.

The strategic reset. Stellantis sold its 49 percent stake in the Canadian battery joint venture with LG Energy Solution. It canceled the new electric Ram pickup, eliminated Jeep and Chrysler PHEV models, and is doubling down on the return of the V8 HEMI for Ram trucks. The declared objective had been 100 percent EV sales in Europe and 50 percent in the US by 2030. Today EVs represent 19.5 percent of sales in Europe and 7.7 percent in the US. The signals were there. Downgrades from Wall Street Zen and Morgan Stanley came on January 31 and February 3 respectively, days before the collapse. The market had already responded. Management ignored the signal for too long.

The lesson for Procurement: building a supply chain on optimistic forecasts without exit triggers is a bet, not a strategy. When real demand diverges from plan, suppliers pay first through unilateral cancellations, forced compensation and specialized capacity that becomes unusable overnight. Do your multi year contracts include flexibility clauses, or are you assuming business forecasts will never change?

🔗 Sources: AXIOS, PR Newswire

💬 Your opinion matters

Do you have feedback to share?

Write to us 📨 at compribene@compri.ai and let us know what you think. We are here to listen and make Compri Bene increasingly useful and relevant. ⚡

Compri Bene is the newsletter by compri.ai that gives Procurement teams superpowers, with the latest news from the world of sourcing, from regulatory changes to industry best practices.

Team Compri

Join compri,

10X your procurement team.

compri uses AI to make your procurement experience easier, faster and smarter. Get in touch to know more